여러분이 홈카지노에서 특별한 혜택을 받을 수 있게 해주는 가입 코드를 제공하고 있습니다. 온라인 카지노 게임에 관심이 있으시다면, [홈카지노공식주소]에서 받을 수 있는 우리의 고유 가입 코드를 사용해 보세요. 이를 통해 특별한 보너스와 혜택을 경험할 수 있습니다. 지금 가입 코드를 이용하세요!

가입코드 혜택 안내

가입코드 혜택 안내

- 신규 가입자 혜택:

- [홈카지노공식주소]에서 받으실 수 있는 가입코드(추천코드)를 사용해 아래 버튼으로 공식 홈페이지에 접속하세요. 가입자에게는 특별한 보너스 혜택이 있습니다.

- 충전 시 추가 혜택:

- 회원 가입 시 가입코드를 입력하신 분들은 홈카지노에서의 게임 머니 충전 시 추가적인 혜택을 경험하실 수 있습니다!

- 이벤트 참여 기회:

- 가입코드를 사용해 참여하는 다양한 이벤트들에서 특별한 보상을 얻을 수 있는 절호의 기회를 잡으세요.

가입코드 받는 방법

가입코드 받는 방법

- 홈 공식 사이트 접속: 아래 버튼을 사용해 공식 사이트에 접속하시면, 회원 가입이나 로그인을 할 때 가입코드를 별도로 입력할 필요가 없습니다.

- (만약, 가입코드가 작동하지 않을 경우) 내 계정 페이지로 이동: 가입코드는 내 계정 페이지에서 확인 및 복사하실 수 있습니다. 더 자세한 사항이 궁금하시면 고객센터로 연락주세요.

- 가입 시 입력: 가입하거나 충전할 경우, 입력란에 가입코드를 정확히 입력하시기 바랍니다.

홈카지노 플레이를 위해 공식주소에서 가입코드나 추천코드를 제공하여 플레이어에게 더 많은 혜택을 제공합니다. 이 코드를 이용하면, 라이브 게임을 언제든지 즐길 수 있게 됩니다. 가입코드를 사용해 바로 라이브 게임에 참가해 보세요!

가입코드 사용 시, 언제든지 특별한 혜택을 받으며 라이브 게임을 즐길 기회를 얻을 수 있습니다. 홈카지노에서는 다채로운 게임 옵션을 제공합니다!

가입코드로 라이브 게임 상시 접속 혜택

- 24/7 라이브 게임:

- 언제 어디서나 홈카지노의 카지노 게임들에 라이브로 참여하고 싶으시다면 가입코드를 활용하세요. 실제 딜러와 함께할 수 있는 기회를 제공합니다.

- 다양한 게임 옵션:

- 다채로운 라이브 게임이 준비되어 있습니다, 블랙잭이나 룰렛, 바카라 등을 포함해 여러분의 취향에 맞게 선택해 보세요.

- 실제 딜러와 대화:

- 실시간 채팅 기능을 이용해 딜러와 직접 대화하며, 라이브 게임을 보다 즐겁게 즐길 수 있습니다. 게임의 즐거움을 극대화하십시오.

가입코드로 접속해 라이브카지노 즐기는 방법

- 가입코드 획득: 공식 주소에서 확인할 수 있는 가입코드를 살펴보십시오.

- 게임 로비 접속: 공식 애플리케이션 또는 사이트를 통해 로비 접속을 시도하세요.

- 가입코드 입력: 게임에 참여하시거나 로그인하실 때 가입코드를 정확하게 입력하세요.

- 라이브 게임 즐기기: 가입코드를 입력하여 라이브 게임에 항상 접속할 수 있고, 실시간으로 열리는 게임을 즐기세요.

지금 바로 [게임 이름]의 라이브 게임을 즐기세요!

가입코드 사용 시, 언제든지 특별한 혜택을 받으며 라이브 게임을 즐길 기회를 얻을 수 있습니다. 홈카지노에서는 다채로운 게임 옵션을 제공합니다!

홈카지노 공식주소를 통해 카지노를 즐기길 원하는 여러분께, 특별 가입 코드를 제공하고 있습니다. 이 코드로 언제 어디서든 다양한 머신 게임을 즐기실 수 있습니다. '게임 시작하기'를 클릭하셔서 가입 코드를 바로 받아 게임에 참여해보세요!

슬롯머신 게임의 다양한 테마를 경험하고 싶으시다면, 가입코드로 언제든 접속하세요! 홈카지노는 언제나 여러분에게 특별한 즐거움을 제공할 준비가 되어 있습니다.

가입코드로 머신 게임 상시 접속 혜택

- 다양한 슬롯 머신 게임:

- 홈카지노에서는 개성 있는 다양한 테마와 스타일의 슬롯 머신 게임을 제공하여, 여러분이 좋아하는 게임을 찾을 수 있습니다.

- 새로운 게임 추가:

- 가입코드로 지속적으로 접속해 있으면, 머신 게임의 새로운 버전이나 테마가 업데이트 될 때 그 순간을 놓치지 않고 바로 플레이할 기회를 갖게 됩니다.

- 특별 보너스 이벤트 참여:

- 여러분이 가입코드를 통해 참여하는 이벤트에서 특별한 보너스를 받을 수 있는 기회를 제공합니다.

가입코드로 접속해 슬롯머신 즐기는 방법

- 가입코드 획득: 공식 주소에 접속해 제공되는 가입코드를 확인하십시오.

- 게임 로비 접속: 공식 애플리케이션 또는 웹사이트를 통해 게임 로비에 들어가세요.

- 가입코드 입력: 게임 참여 또는 로그인 시에는 가입코드를 올바로 입력해야 합니다.

- 머신 게임 즐기기: 언제든지 가입코드를 이용해 다채로운 슬롯머신 게임을 경험하세요.

지금 바로 슬롯머신 게임을 상시로 즐기세요!

슬롯머신 게임의 다양한 테마를 경험하고 싶으시다면, 가입코드로 언제든 접속하세요! 홈카지노는 언제나 여러분에게 특별한 즐거움을 제공할 준비가 되어 있습니다.

여러분이 홈카지노에서 제공하는 특별 가입코드로 다양한 스포츠에 베팅할 수 있습니다. 어디에 계시든 가입코드로 스포츠 베팅의 흥미를 발견해 보세요!

가입코드를 이용하여 상시로 스포츠 베팅을 즐기며, 다양한 경기에 참여하세요. 여러분의 즐거움을 위해 항상 특별한 것을 제공하고 있습니다!

가입코드로 상시 스포츠 베팅 혜택

- 다양한 스포츠 경기:

- 여기에서는 축구, 농구, 야구, 테니스를 포함한 다양한 스포츠 종목에 대한 베팅 기회를 제공하고 있습니다.

- 실시간 베팅 옵션:

- 가입코드로 접속을 유지하면, 실시간 경기 베팅 옵션을 놓치지 않고 이용할 수 있습니다.

- 특별 베팅 이벤트 참여:

- 가입코드를 활용해 참가하는 여러 이벤트에서는 특별 베팅 보너스를 얻을 수 있는 특별한 기회가 있습니다.

가입코드로 접속하는 방법

- 가입코드 획득: 공식 홈카지노 주소를 방문해 제공되는 가입코드를 확인하세요.

- 게임 로비 접속: 공식 앱이나 사이트를 통해서 게임 로비에 접속하십시오.

- 가입코드 입력: 로그인할 때나 베팅에 참여할 때는 가입코드를 올바르게 입력하세요.

- 스포츠 베팅 시작: 스포츠 베팅을 상시로 시작하고 싶다면, 가입코드를 활용해 다양한 경기에 베팅하십시오.

지금 [게임 이름]의 스포츠 베팅을 상시로 즐기세요!

가입코드를 이용하여 상시로 스포츠 베팅을 즐기며, 다양한 경기에 참여하세요. 여러분의 즐거움을 위해 항상 특별한 것을 제공하고 있습니다!

여러분이 언제든지 다양한 미니게임을 즐길 수 있도록 [게임 이름에서 특별한 가입 코드를 제공합니다. 지금 바로 이 코드로 [게임 이름의 재미있는 미니게임을 시작해 보세요!

가입코드를 활용하여 언제나 다양한 장르의 미니게임을 플레이하고, 홈카지노에서 여러분을 위한 풍부하고 다채로운 게임 세계를 경험하세요!

가입코드로 상시 미니게임 혜택

- 다양한 미니게임:

- 퍼즐, 아케이드, 카지노를 포함한 다양한 장르의 미니게임을 여러분께 제공합니다. 기호에 맞게 게임을 선택하여 즐겨보세요.

- 새로운 게임 추가:

- 가입코드로 접속해 있으면 새로운 미니게임이 추가될 때마다 바로 플레이할 수 있는 기회를 손에 넣을 수 있습니다. 이 기회를 잡으세요.

- 특별 보너스 이벤트 참여:

- 다양한 이벤트 참여 시 가입코드를 통해, 특별 미니게임 보너스 획득 기회가 주어지니 이를 활용하세요.

가입코드로 접속하는 방법

- 가입코드 획득: 홈카지노공식주소에서 확인할 수 있는 가입코드를 확인해 보세요. 지금 바로 방문하세요.

- 게임 로비 접속: 게임 로비 접속을 위해서는 공식 사이트나 앱을 이용해 보세요.

- 가입코드 입력: 미니게임 참여나 로그인할 때 정확한 가입코드 입력이 필요합니다.

- 미니게임 즐기기: 가입코드를 사용하여 언제든지 여러 미니게임을 플레이하며 기억에 남는 경험을 하세요.

지금 [게임 이름]의 미니게임을 상시로 즐기세요!

가입코드를 활용하여 언제나 다양한 장르의 미니게임을 플레이하고, 홈카지노에서 여러분을 위한 풍부하고 다채로운 게임 세계를 경험하세요!

홈카지노 신규가입 안내

홈카지노의 새 가족 여러분께 환영의 인사를 전합니다! 우리의 모험에 함께하시게 되어 영광입니다. 최근에 블랙유저들의 비윤리적인 활동, 특히 계좌번호 팔이가 증가함에 따라, 모든 사용자에게 보다 안전하고 즐거운 환경을 제공하기 위한 조치들을 실시하기로 했습니다. 신규 가입 과정을 마치기 위해 아래 안내 사항을 반드시 확인해주세요.

신규가입 안내사항

신규가입 안내사항

- 정확한 기재가 필요합니다:

- 가입을 마친 이후에 제공되는 모든 정보란에 정확한 내용을 기재해야 합니다. 올바른 정보 제공으로 서비스 이용에 도움을 주세요.

- 다음 날 승인 전화 진행:

- 가입이 끝난 다음 날, 승인을 위한 전화 연락을 받으실 예정이고, 상담원과의 대화를 통해 서비스를 더욱 안전하게 이용할 수 있습니다.

- 질문 사항에 대한 답변:

- 승인을 위한 전화 도중 몇 가지 중요한 질문에 대해 정확히 답해주십시오. 이런 절차는 모든 회원을 블랙유저로부터 보호하는 데 목적이 있습니다.

- 본인확인 완료 후 승인:

- 모든 절차를 완료하고 본인 확인을 마치면 승인을 받을 수 있습니다. 이를 통해 여러 게임과 이벤트에 참여할 수 있는 자유를 얻게 됩니다.

홈 카지노 사이트 이벤트 안내

여러분의 중요한 순간들을 더욱 풍요롭게 만들기 위해, 홈카지노는 여러 가지 이벤트를 준비했습니다. 함께하는 모든 순간이 즐거움과 행운으로 가득 차기를 바라며, 현재 개최 중인 주요 이벤트 정보는 아래에 안내되어 있습니다.

홈카지노에서는 여러분을 위한 다양한 혜택을 지속적으로 제공 중입니다. 게임 내 이벤트 영역에서 자세한 사항을 확인하실 수 있습니다. 흥미로운 게임과 이벤트로 여러분의 참여를 기다립니다!

감사합니다. 함께 특별한 순간을 즐겨보세요!

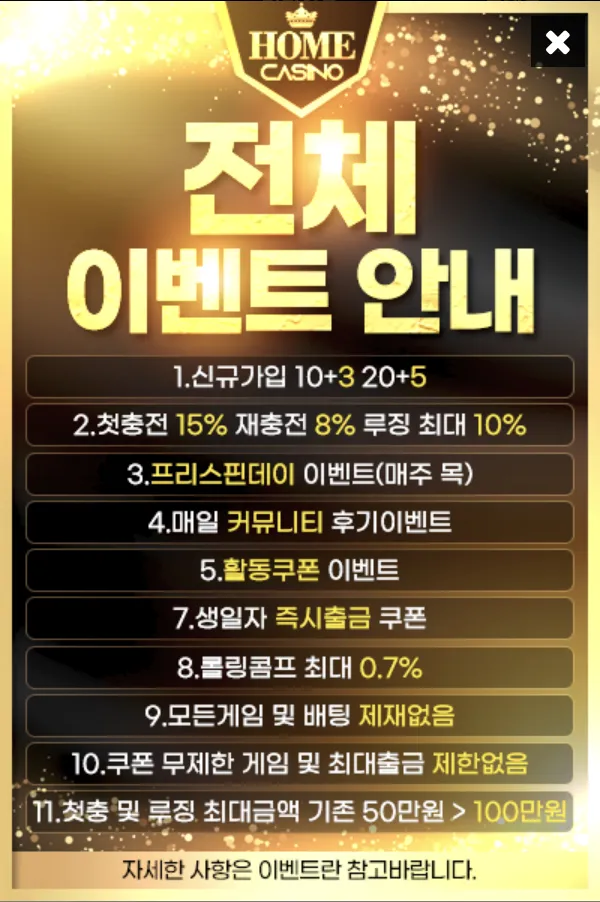

현재 진행 중인 주요 이벤트

현재 진행 중인 주요 이벤트

- 신규가입 이벤트:

- 새롭게 가입하신 분들께는 10+3과 30+5의 추가 보너스를 제공해, 게임 시작을 더욱 멋지게 만들어 드립니다.

- 충전 시 추가 혜택:

- 첫 충전 시 여러분에게 15%의 보너스를, 그리고 다시 충전하실 때마다 8%의 추가 보너스를 지급하여 게임의 재미를 배가시킵니다.

- 루징 보상 이벤트:

- 게임에서 패배할 시에도, 최대 10%의 보상을 드려 패배를 값진 경험으로 바꿔드립니다.

- 프리스핀데이 매주 목요일 개최:

- 매주 목요일마다 진행되는 프리스핀데이에 모든 사용자들이 혜택을 받을 수 있으니, 이 기회를 절대 놓치지 마세요.

- 커뮤니티 후기 이벤트:

- 매일 열리는 커뮤니티 후기 이벤트에서 여러분의 생생한 리뷰를 보상으로 존중해 드립니다.

- 활동쿠폰 이벤트 제공:

- 다양한 활동쿠폰 이벤트에서 제공하는 특별한 혜택을 받아보세요.

- 생일 축하 쿠폰 제공:

- 생일을 맞은 플레이어들에게는 출금이 가능한 특별한 쿠폰을 선물로 증정합니다.

- 롤링콤프 혜택:

- 여러분의 게임이 더 유리해질 수 있도록 최대 0.7%의 롤링콤프를 제공합니다.

- 무제한 쿠폰 및 출금 혜택:

- 제한 없이 사용 가능한 모든 쿠폰과 최대 출금 제한 없이 자유롭게 즐기실 수 있습니다.

자세한 내용은 이벤트 란에서 확인하세요!

홈카지노에서는 여러분을 위한 다양한 혜택을 지속적으로 제공 중입니다. 게임 내 이벤트 영역에서 자세한 사항을 확인하실 수 있습니다. 흥미로운 게임과 이벤트로 여러분의 참여를 기다립니다!

감사합니다. 함께 특별한 순간을 즐겨보세요!

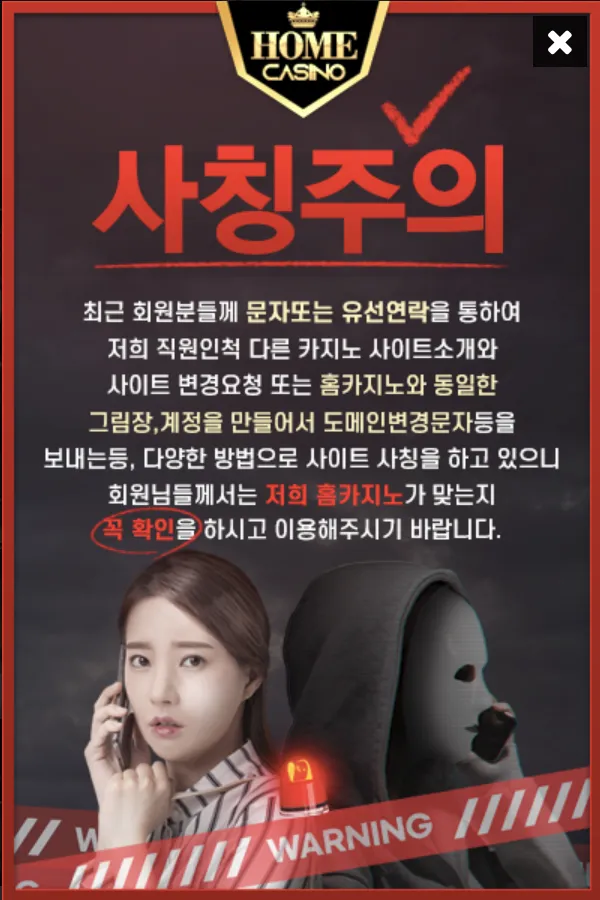

홈 카지노 사칭주의

홈 카지노 사칭주의

소중한 홈카지노 플레이어 여러분에게 인사드립니다! 최근 문자나 전화를 통한 사칭으로 다른 카지노로의 전환 유도가 증가하고 있습니다. 이에 따라, 여러분의 개인 정보와 자산 보호를 위해 각별히 주의해 주시길 바랍니다.

주의사항

주의사항

- 문자 및 유선 연락 주의:

- 홈카지노 사칭 연락이 오는 경우, 바로 행동에 옮기지 말고 세심하게 확인해보세요.

- 이전 유도에 주의:

- 다른 카지노로 이동하라는 제안을 받게 될 경우, 그 제안에 바로 응하지 말고 세부 사항을 꼭 확인해 주세요.

- 정품 사이트 확인:

- 사용하시기 전 공식 사이트의 주소를 꼭 확인해주시기 바랍니다. 피싱 사이트는 공식 사이트와 유사한 주소를 사용해 사용자를 기만할 수 있습니다.

- 고객센터로 문의:

- 만약 의심스러운 연락이나 사이트를 발견하셨다면, 공식 웹사이트의 고객센터로 문의해 주세요.

여러분의 안전이 최우선입니다

여러분의 안전이 최우선입니다

게임을 안전하게 즐기실 수 있도록 전력을 다하고 있지만, 피싱과 같은 악의적 시도가 여러분의 안전을 위협할 수 있습니다. 여러분의 정보와 자산 보호를 위해 항상 경계하십시오.